It couldn’t possibly be more of a disparate tale between Intel and AMD: Intel’s earnings last week found the company announcing that it faces a delay to its 7nm process node until 2023, sending the stock plummeting 16% in spite of its solid financials. In contrast, AMD’s stock soared to record highs on the news of its stellar financial performance and on-track execution for its next-gen Milan CPUs, Zen 3 consumer processors, and RDNA 2 GPUs, all of which come to market later this year. AMD’s stock reached a record $74.47, a 9.9% jump in after-hours trading (at the time of writing).

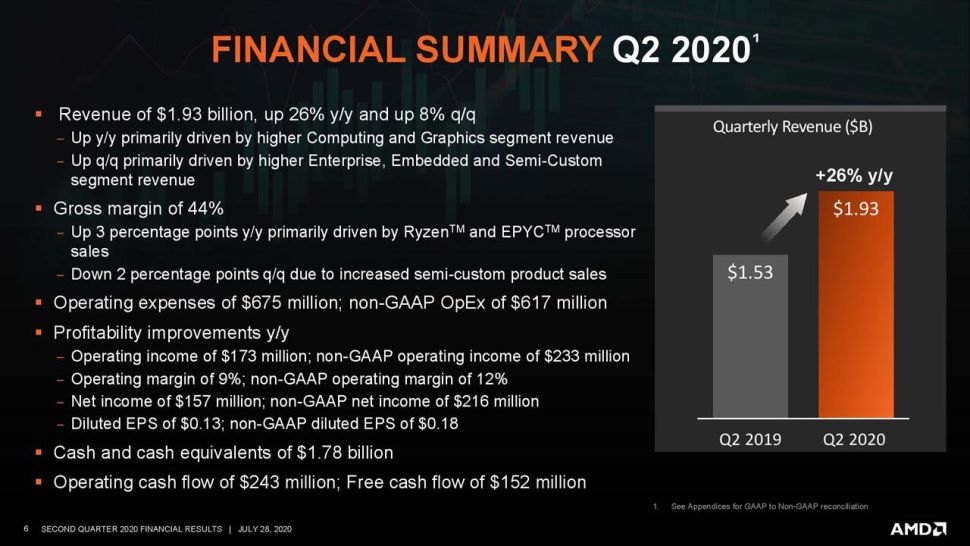

AMD reported record revenue of $1.93 billion (up 26% YoY), along with record notebook and EPYC CPU sales in its 2Q 2020 earnings report today. AMD also notched a 12-year high in consumer processor sales as its client computing group notched 45% growth propelled in part by doubled sales of notebook processors. AMD CEO Lisa Su also said the company had doubled its EPYC sales and reached its target of double-digit server market share as the segment reached 20% of AMD’s overall second-quarter revenue.

Even more telling, the company raised its full-year revenue projections from 25% growth to 32% on the back of continued growth in the key PC, data center, and gaming segments. The company earned $157 million in profit for the quarter, a marked increase over the $35 million from a year prior. AMD’s margins weighed in at 44%, a 2% sequential decline but 3% improvement year over year.

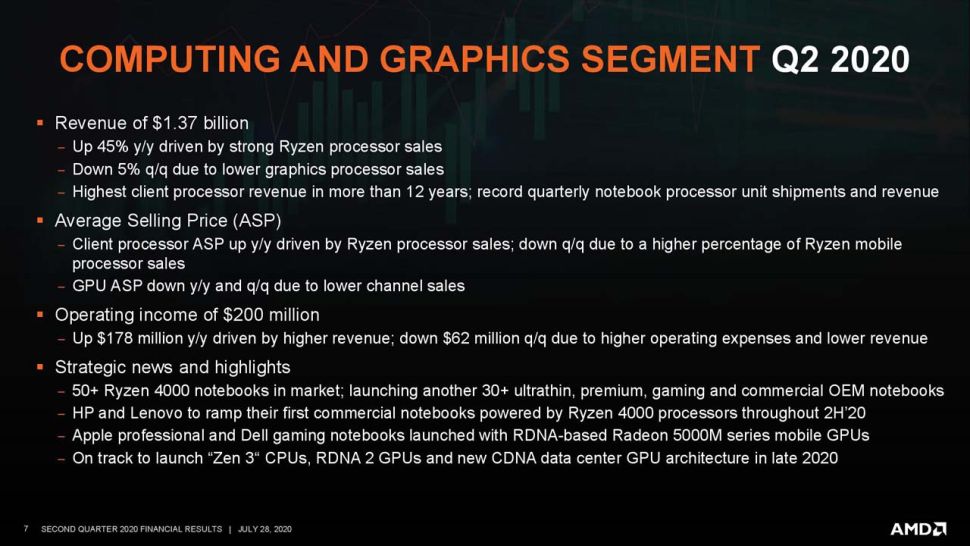

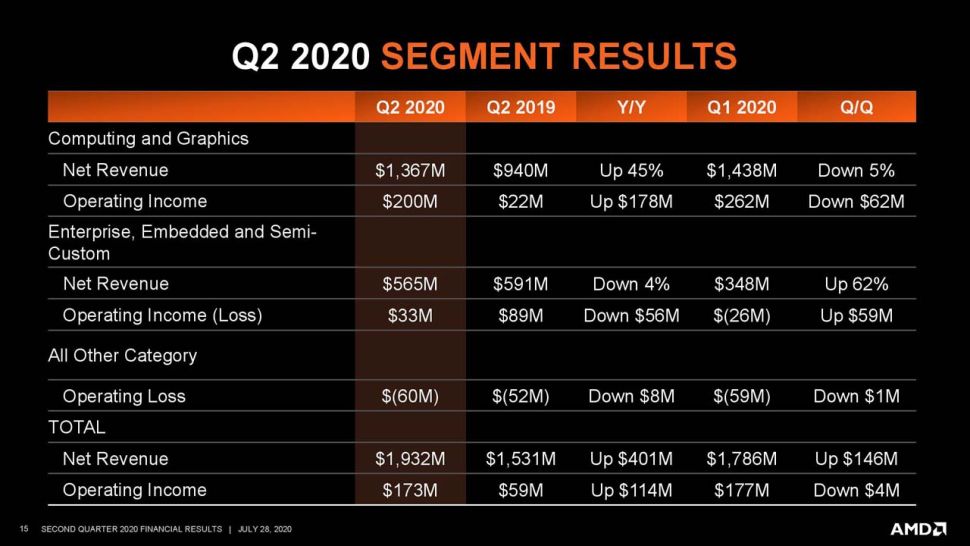

AMD’s Computing and Graphics revenue grew 45% year-over-year to $1.37 billion on strong Ryzen sales despite lower graphics sales. AMD reported its highest consumer CPU revenue in 12 years, but much of the gain came on the back of AMD’s Ryzen 4000 processors for laptops. AMD’s mobile processor sales doubled YoY and the 50+ notebooks on the market will be joined by another 30+ models by the end of the year. The mobile segment comprises roughly 65% of the total client CPU market, so these gains are important as Intel preps to release its 10nm Tiger Lake models later this year.

Meanwhile, AMD’s desktop CPU sales declined compared to the previous quarter, but increased year over year. Sales of more expensive models also led to improved average selling prices (ASPs). Su noted that the company has it’s first Zen 3 processors for the consumer market coming later this year.

AMD’s discrete GPU sales and ASPs also declined, which was partially offset by increased mobile graphics sales (up double-digits). Su also said the company remains on track for its launch of the RDNA 2 “Big Navi” graphics cards later this year, commenting that “I think it’s a full refresh for us from the top of the stack through the rest of the stack”

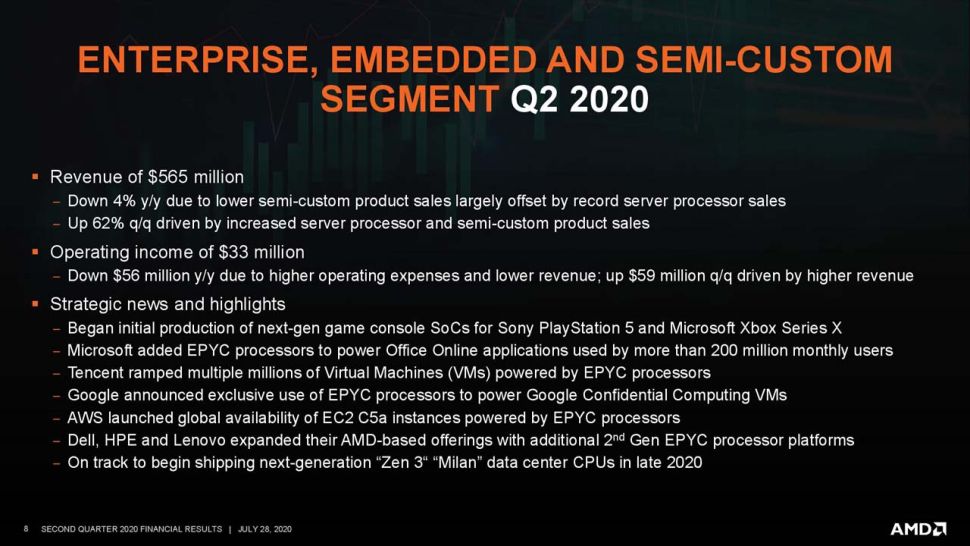

AMD’s data center EPYC sales set a quarterly record and doubled year-over-year as the Enterprise, Embedded and Semi-Custom group delivered $565 million in revenue. For comparison, Intel’s data center group recorded $7.1 billion last quarter, which highlights why investors are so optimistic about AMD’s gains in the server market, especially in light of Intel’s looming process delays.

AMD said it has reached its goal for a double-digit percentage of the server CPU market. However, while AMD has eclipsed that number, the company doesn’t include several large segments in its accounting of server share, instead focusing solely on single- and dual-socket servers.

The company didn’t set a new goal for market share penetration, but predicts accelerating uptake of its data center CPUs in the back half of the year. Su stated at a recent investor event that the company wouldn’t project server CPU sales based on market share in the future, instead focusing on revenue targets: “I think as we go through the second quarter and the second half of the year, we’re going to transition from share targets to more of a percentage of AMD revenue because that will give you a better idea of the progression. […] So the server business will continue to be very strategic. I probably won’t give you another share target. But what we did say, though, and it gives you an idea of what we think the size of the business can be, when we did our Financial Analyst Day a couple of months ago, we said we saw the server – or the data center business for us, being upwards of 30% of overall AMD.” During today’s earnings call, Su noted that EPYC comprised 20% of the company’s revenue, so it’s clear the company has plans for significantly more uptake.

AMD’s data center GPU sales also declined on the quarter, which the company hopes will improve as its CDNA 2 graphics accelerators arrive later in the year. AMD’s semi-custom business continues to recede as it prepares for the ramp of the Microsoft Xbox Series X and Sony PS5 that land later in the year. Those products should also help improve sales and margins.

Looking forward to the remainder of the year, AMD predicts that it will continue to grow share in the Desktop PC and notebook markets and guided for $2.55 billion in revenue for Q3, an increase of 42% YoY.